1.1 Introduction

What is an Economy?

An economy is a system that organizes the production, distribution, and consumption of goods and services within a region (for example, a country). It basically describes how a society decides what to make, how to make it, and who gets the output.

The Three Vital Processes of an Economy:

Every economy on the planet relies on three core activities to actually function and survive:

- Production: The process of turning raw inputs (like land, labor, and capital) into useful goods and services.

- Distribution: The process of moving these goods and services through markets so they reach the people who need them.

- Consumption: The process where individuals and households actually buy and use up these goods and services to satisfy their wants.

Why do we study Economics?

We study economics because of one giant, unavoidable headache: Scarcity.

Human wants and needs are completely unlimited, but the resources needed to satisfy them (time, money, labor, land, and materials) are strictly finite and limited.

The Solution: Because we can't have everything we want, individuals, businesses, and governments are forced to make choices. Economics is simply the study of how we make those choices to allocate our scarce resources as efficiently as possible.

1.2 Scarcity

What is Scarcity?

Scarcity is the basic economic problem that arises because people have unlimited wants but resources are limited. Because resources are scarce, they cannot satisfy every human need and want simultaneously.

It doesn't matter if you’re a broke college student or a billionaire; nobody can have everything. Time, money, land, and labour are all limited.

The Real Twist: Alternative Uses

Here is the thing: scarcity by itself isn't the only issue. The real headache is that resources have alternative uses. This means a single resource can be used for different purposes.

If a resource only did one thing, life would be simple. But because it can do multiple things, you have to prioritise.

Real-World Examples:

- The Land Example: A piece of land is scarce. But it also has alternative uses. A farmer can use it to grow wheat, OR use it to build a factory, OR use it to build a school. If he chooses the school, he loses out on the wheat and the factory.

- The Money Example: You have a $20 bill (scarce resource). It has alternative uses: you can spend it on a movie ticket, buy a textbook, or grab lunch. Buying the movie ticket means giving up the textbook and lunch.

- The Time Example: You have 2 hours of free time tonight. You could study for your economics exam, stream a show, or sleep.

1.3 Economic Problem

What is the Economic Problem?

The economic problem is the problem of choice, which arises because people have unlimited wants but resources are limited. Because resources are scarce and have alternative uses, individuals, businesses, and governments have to choose which wants to satisfy and which ones to leave unfulfilled.

Basically, it is the challenge of deciding how to allocate our limited resources to meet our unlimited wants as efficiently as possible.

Reasons for the Economic Problem

The economic problem doesn't just happen by accident. It is caused by three specific, unavoidable conditions that exist in every society:

- Unlimited Human Wants Human wants and needs are completely endless. As soon as one want is satisfied, a new one takes its place. On top of that, wants multiply over time due to changes in technology, fashion, and lifestyle. Because they are infinite, no society can ever produce enough to satisfy every single person's desires.

- Scarcity of Resources The resources needed to satisfy human wants such as land, labor, capital, and time; are strictly finite and limited in supply. Demand for these resources is always greater than their availability, which means scarcity is a permanent reality.

- Alternative Uses of Resources To make matters more complicated, resources aren't just scarce; they also have alternative uses. A single resource can be used for different purposes. Example: A piece of land can be used to grow crops, build a factory, or construct a hospital.

Mnemonic: USA (Unlimited human wants; Scarce Resources; Alternative Uses)

1.4 Meaning of Economics

Economics is a social science that studies how individuals, businesses, governments, and nations make choices about how to allocate scarce resources. It focuses on how these resources are used to satisfy unlimited human wants. Economics is all about making choices in the presence of scarcity.

1.5 Positive and Normative Economics

1. Positive Economics: Positive economics deals with objective, testable statements. It focuses on pure facts and can be proven right or wrong using data.

- Example: “If a tax is imposed on sugar, the price of soda will rise." (This can be tested and proven with data).

2. Normative Economics: Normative economics deals with subjective statements and opinions. It focuses on value judgments and what people think should happen. You cannot prove it true or false.

- Key Words: Look for words like should or ought to.

- Example: "The government should tax sugar to make people healthier." (This is an opinion on what is right or fair).

Mnemonic: Check the first letters to tell them apart:

- Positive = Proven facts

- Normative = Not provable (Opinions)

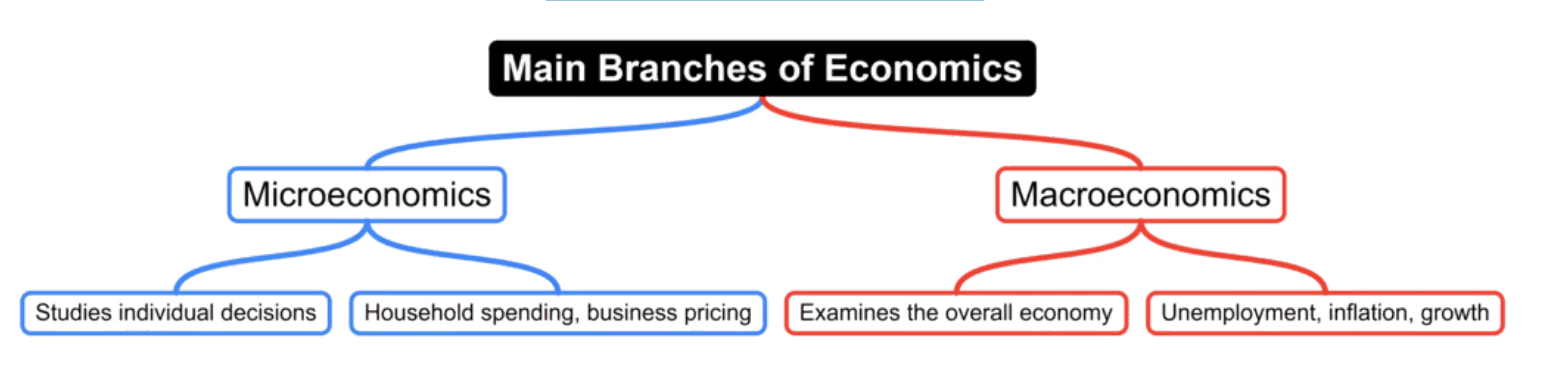

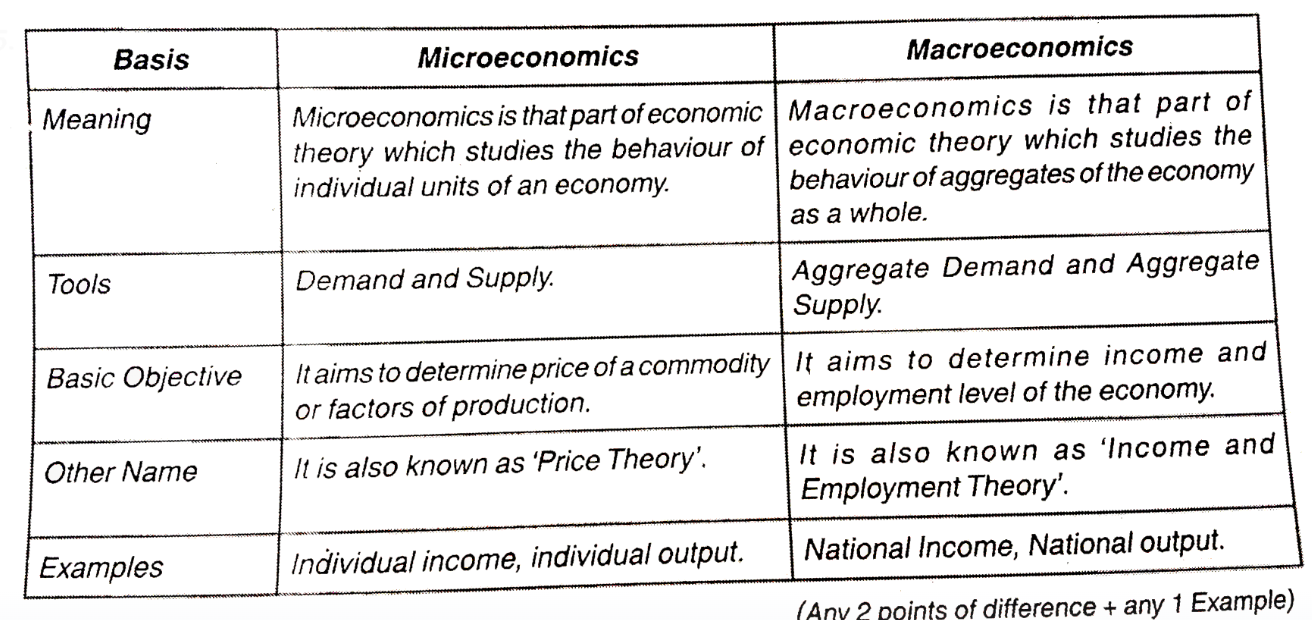

1.6 Microeconomics and Macroeconomics

The study of economics is divided into two major branches. At a glance, Microeconomics is often called Price Theory, while Macroeconomics is known as Income and Employment Theory.

Mnemonic: The Lens Focus Look through a MIcroscope lens to study Individual units (like Individual prices and firm outputs), or zoom out with a MAcro camera lens to study Aggregates (like All national income and Aggregate demand/supply).

1. Core Definitions and Origins

Microeconomics (Price Theory)

- Origin of the Word: Derived from the Greek word 'Mikros', which means small.

- Definition: Microeconomics is that part of economic theory which studies the behavior of individual units of an economy, such as an individual consumer, a single household, a specific firm, or a particular industry.

- Core Focus: It focuses on how individual prices are determined and how resources are allocated among specific goods and services. Hence, it is widely known as Price Theory.

Macroeconomics (Income Theory)

- Origin of the Word: Derived from the Greek word 'Makros', which means large.

- Definition: Macroeconomics is that part of economic theory which studies the behavior of aggregates of the economy as a whole, such as national income, total employment, aggregate savings, and general price level.

- Core Focus: It focuses on how the overall level of national income and employment is determined in a country. Hence, it is widely known as Income and Employment Theory.

2. Difference Between Microeconomics and Macroeconomics

3. Interdependence of Micro and Macro

Microeconomics and Macroeconomics are not completely separate; they constantly affect one another. You cannot fully understand one without the other.

Micro Depends on Macro: Decisions made by a single person or business (Micro) are heavily influenced by the state of the whole economy (Macro).

- Simple Example: A local shop owner wants to borrow money to expand their store (Micro decision). Whether they actually do it depends on the national interest rates set by the central bank and the country's inflation rate (Macro factors).

Macro Depends on Micro: What happens in the entire economy (Macro) is just the sum total of millions of individual decisions (Micro).

- Simple Example: National Income (Macro) is calculated by adding up the individual incomes (Micro) earned by every single worker and business owner in the country. If individuals stop making money, the nation's total income drops.

4. Micro-Macro Paradoxes (The Paradox of Thrift)

An economic paradox happens when something that works perfectly for one person turns into a total disaster when everyone does it.

- At the Micro Level (Individual): Saving money is smart. If you save more money, you build up your personal bank account and secure your future.

- At the Macro Level (The Whole Economy): If every single person in the country decides to save all their money at the same time, it crashes the economy.

Why does this happen? When everyone hoards money, spending drops to zero. Your spending is someone else's income, a drop in spending means businesses stop making money. Stores close down, factories lay off workers, and unemployment skyrockets. In the end, because everyone lost their jobs, total national savings actually go down instead of up.

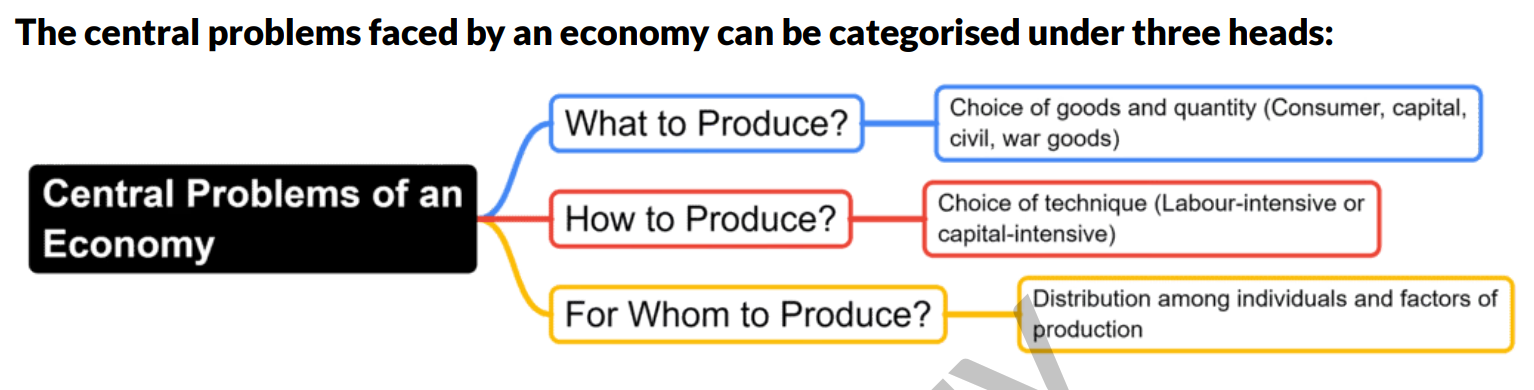

1.7 Central Problems of an Economy

At its core, every economy in the world is just trying to solve one big puzzle: how do we use what we have to give people what they need? Because resources are scarce and have alternative uses, every society faces three central problems. Here is exactly how they work:

Mnemonic: (Who Hacked Will Smith) What, How, Whom.

1. What to Produce?

This is the problem of choosing which goods and services to make, and how much of each to produce. Because resources are limited, you cannot make everything for everyone. If you use your land and factories for one thing, you automatically give up the chance to make something else.

The Two Big Decisions:

- Types of Goods: A society must choose between different categories of goods. Do you produce consumer goods (like food and clothes) or capital goods (like factory machinery)? Do you make civil goods (like bread and hospitals) or war goods (like guns and tanks)?

- Quantity of Goods: Once you pick the goods, you have to decide the exact amount to produce.

- The Goal: Allocate resources to maximise the total satisfaction of society. This means identifying what your people urgently need right now.

- Real-World Example: Think of a country with a tight budget. It has to decide whether to spend its money building schools for the future or buying fighter jets for defense.

2. How to Produce?

This is the problem of choosing the method or technique used to manufacture goods. Once you know what you are making, you have to figure out the most efficient way to put it together without wasting your scarce resources.

The Two Main Techniques:

a) Labor-Intensive Technique (LIT): This method uses more human workers and fewer machines. It is a great option for countries with large populations because it creates jobs and reduces unemployment.

b) Capital-Intensive Technique (CIT): This method uses more modern machines and fewer workers. It is highly efficient, boosts production speed, and helps the economy grow faster, but requires expensive technology.

The Goal: Combine your resources to minimize the overall cost and maximize the total output. You want the cleanest, cheapest, and most productive method available.

Real-World Example: Imagine a clothing brand. It has to decide whether to set up a factory where workers weave clothes using manual handlooms, or a fully automated factory run by high-tech power looms.

3. For Whom to Produce?

Also known as the Theory of Distribution of Income, this is the problem of how the final goods and services are divided among the people. It asks: who gets to enjoy the output of the economy, and how much do they get?

The Two Main Directives:

a) Functional Distribution: This looks at how income is shared among the factors of production that actually helped make the goods. It determines how much rent goes to land, wages to labor, interest to capital, and profit to the entrepreneur.

b) Personal Distribution: This looks at how national income is shared among individual households. It addresses the economic gap between the rich and the poor.

The Goal: Ensure that the urgent needs of all segments of society are met fairly, providing a basic, decent standard of living for every citizen.

Real-World Example: A government must decide whether to let the free market produce luxury cars for high-income earners who can afford them, or use its resources to fund affordable public buses so low-income citizens can get to work.

1.8 Opportunity Cost

Opportunity cost is simply the value of the next best choice you have to give up when you make a decision.

Because you can't do everything or buy everything at once, choosing one option means sacrificing another. The option you didn't choose; your second-best alternative, is your opportunity cost.

2 Simple Examples

1. The Sunday Night Example (Time)

Imagine you have free time on Sunday night. Your top two choices are:

- Studying for your economics test.

- Watching a movie.

If you choose to study, the opportunity cost is the entertainment and relaxation you lost by not watching the movie.

2. The Pocket Money Example (Cash)

You have enough money to buy either a burger or a notebook. You can't afford both.

If you buy the burger, the opportunity cost is the notebook you had to leave behind.

1.9 The Production Possibility Frontier (PPF)

Imagine you have a single plot of land. You can use it to grow wheat, grow cotton, or a mix of both. If you want more wheat, you naturally have to give up some cotton because the land size doesn't change.

The Production Possibility Frontier (PPF) is just a visual map of this.

Definition: The PPF is a curve that shows all the maximum possible combinations of two goods that an economy can produce using its available resources and technology fully and efficiently.

Assumptions of PPF

To look at the pure relationship between choices, we apply Ceteris Paribus (latin for all other things remaining constant) to these five conditions:

- Two Goods: The economy only makes two items (e.g., Wheat and Cotton).

- Fixed Resources: The total amount of land, labor, and capital does not change.

- Full Efficiency: Resources are fully employed with zero waste.

- Constant Technology: The level of technology stays exactly the same.

- Unequal Efficiency: Resources are not equally great at making both items. A master farmer will naturally lose efficiency if you force them to work in a tech factory.

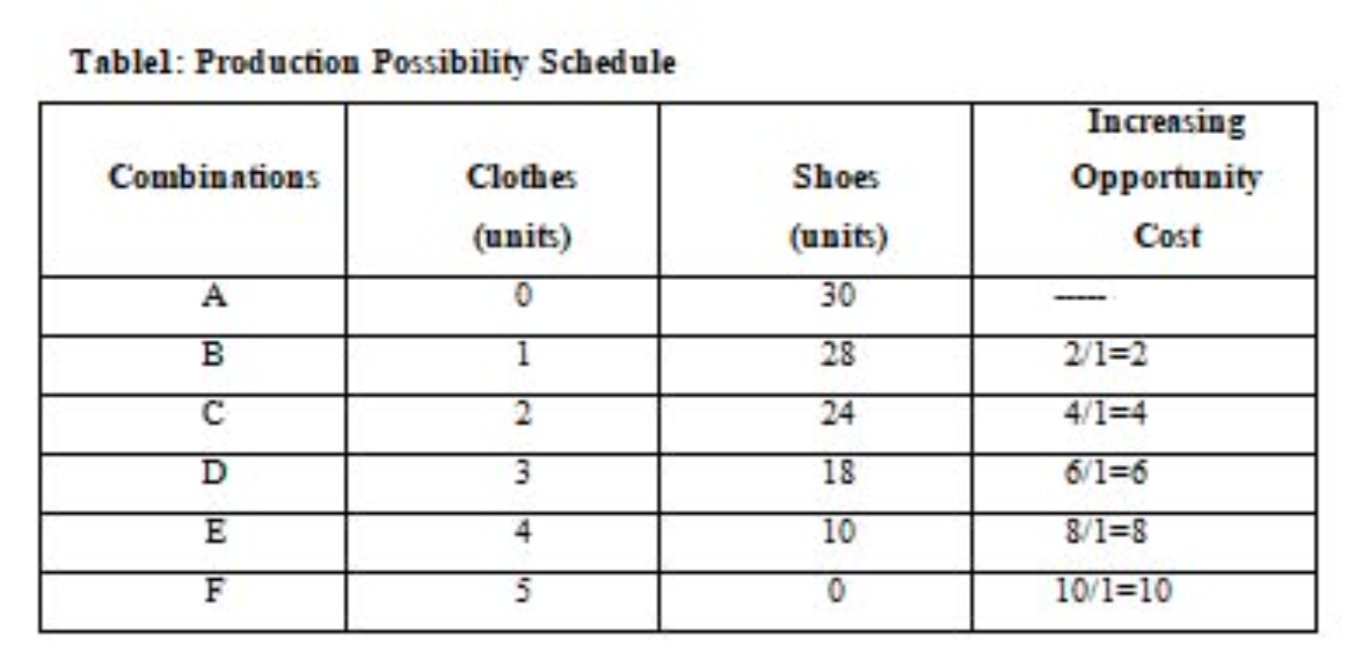

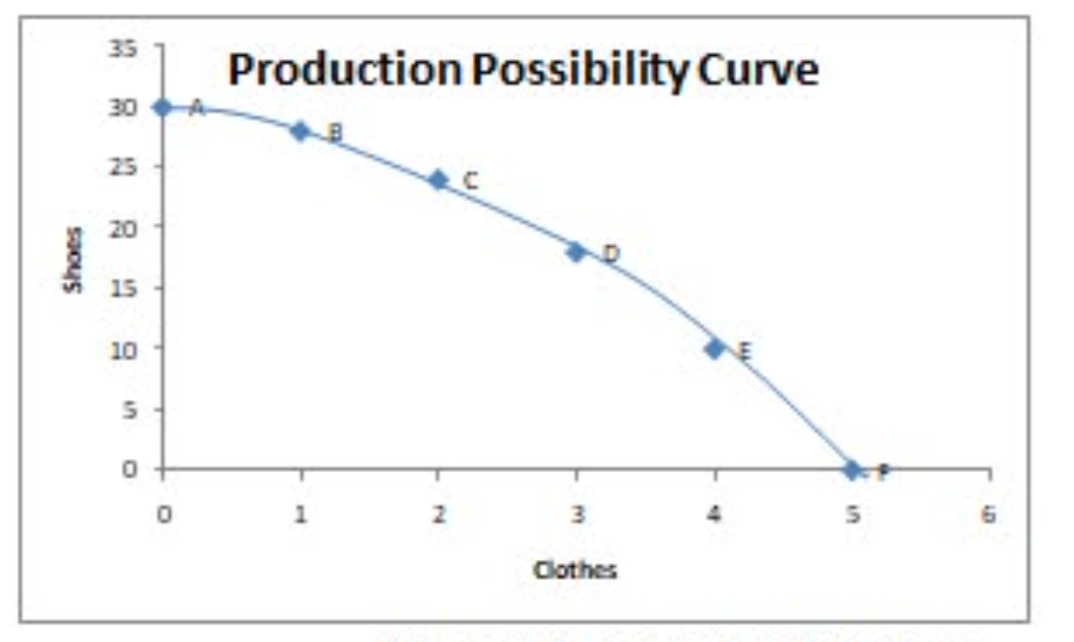

Let’s look at a hypothetical economy producing Shoes and Clothes

If we plot these combinations on a graph, we get a downward-sloping curve that bends outward (concave) from the origin.

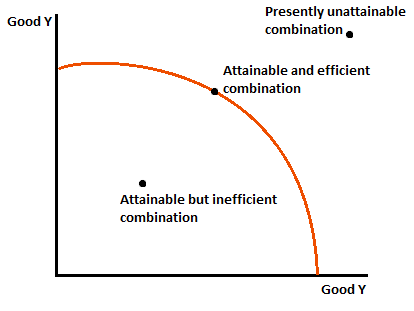

Attainable vs. Unattainable Combinations

Look at your PPF graph like a property boundary line:

- Attainable Points (On or Inside the Curve): Any point sitting directly on the PPF line (like Points A, B, or C) represents efficient production; resources are fully used. Any point inside the curve represents inefficient production or underemployment (e.g., factories running at half capacity or workers being unemployed). The economy can produce here, but it's wasting potential.

- Unattainable Points (Outside the Curve): Any point sitting outside the line is physically impossible to reach right now because the economy simply does not have enough resources or advanced enough technology to produce that much stuff.

Will an economy always operate ON the PPF?

No, not necessarily. The PPF shows the maximum potential. If an economy suffers from recessions, strikes, mass unemployment, or natural disasters, it will operate inside the PPF curve due to wasted or idle resources.

Why does the PPF look the way it does?

It comes down to two closely related concepts: Marginal Opportunity Cost (MOC) and the Marginal Rate of Transformation (MRT).

To understand both, let's use a simple example: Imagine a factory that can produce either Smartphones or Laptops. You decide to shift workers away from making laptops to make more smartphones.

Marginal Opportunity Cost:

MOC is the actual amount of a good you lose when you decide to produce one extra unit of another good.

- The Real-World Example: Imagine your workers are currently making 50 laptops. You want to make 1 extra smartphone. To do this, you have to take a worker off the laptop line, causing laptop production to drop to 48. What did that 1 extra smartphone cost you? It cost you 2 laptops. That "2 laptops" is your Marginal Opportunity Cost.

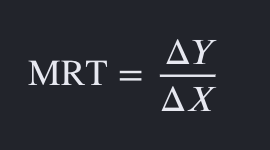

Marginal Rate of Transformation:

MRT is just MOC expressed as a ratio or a rate. It measures the slope of the PPF.

- Continuing the Example: If you sacrifice 2 laptops to get 1 smartphone, the rate of transformation is 2 laptops to 1 smartphone.

Why does MOC increase?

Imagine an economy that only makes guns and butter, where your best worker is currently happily building guns because that is his specialty. If you suddenly decide you need more butter, you have to pull this expert gunsmith away from his weapons bench and put him in a dairy factory instead. Because he has absolutely no experience churning butter, he is going to be clumsy and slow, meaning your gun production drops drastically while your butter production barely goes up at all. This mismatch is exactly why the MOC rises: you are forced to sacrifice a massive, painful amount of guns just to get a tiny, disappointing amount of butter, simply because your workers are specialised and cannot be perfectly swapped from one job to another.

Can the shape of the PPF ever change?

Yes! While the MOC usually increases (making the curve concave), theoretically the PPF can take other shapes based on how resources behave:

1. Can a PPF be a Straight Line? Yes, if the MOC remains constant. This happens only if resources are perfectly adaptable and equally efficient at producing both goods. You sacrifice the exact same amount of Good Y every single time you want another Good X.

2. Can a PPF be Convex to the Origin (Bends Inward)? Yes, if the MOC is decreasing. This is very rare.

Why do economists call the PPF a Transformation Curve?

When you decide to produce more of one good, you don't magically cast a spell to turn a gun into a stick of butter. Instead, you are transforming the use of your resources. By taking a factory worker off the weapon assembly line and putting them into a dairy factory, you have effectively "transformed" guns into butter. This is why it is called a Transformation Curve.

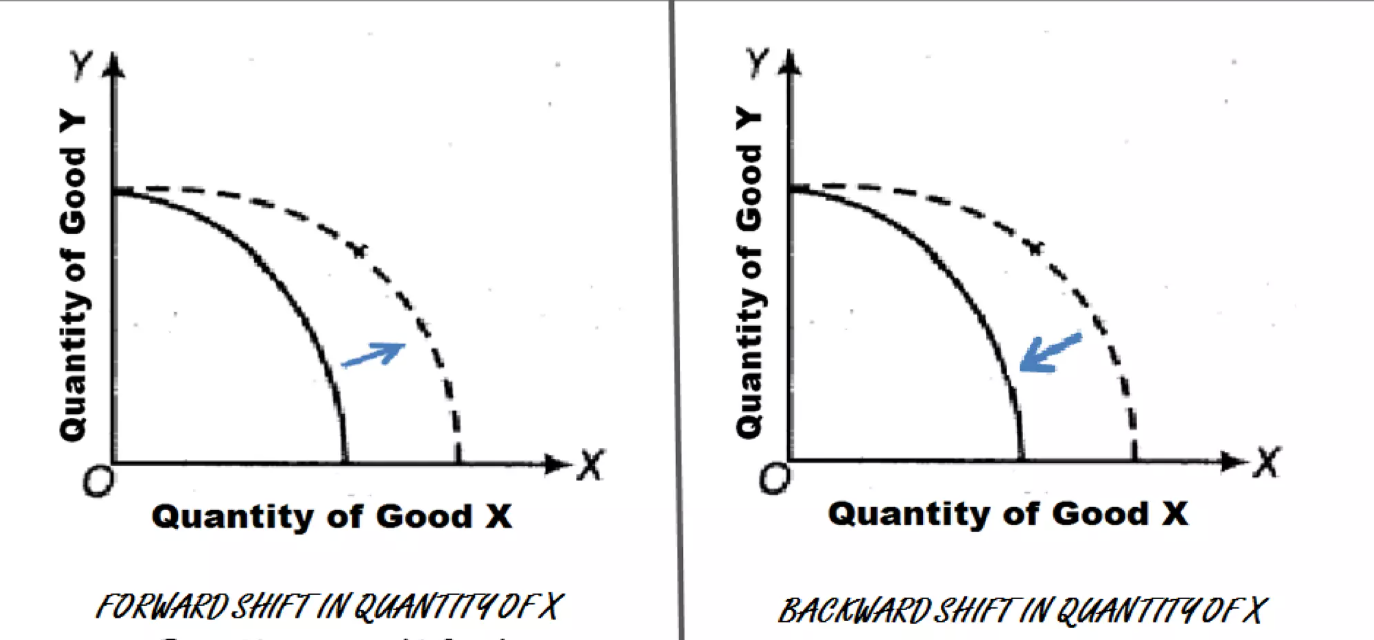

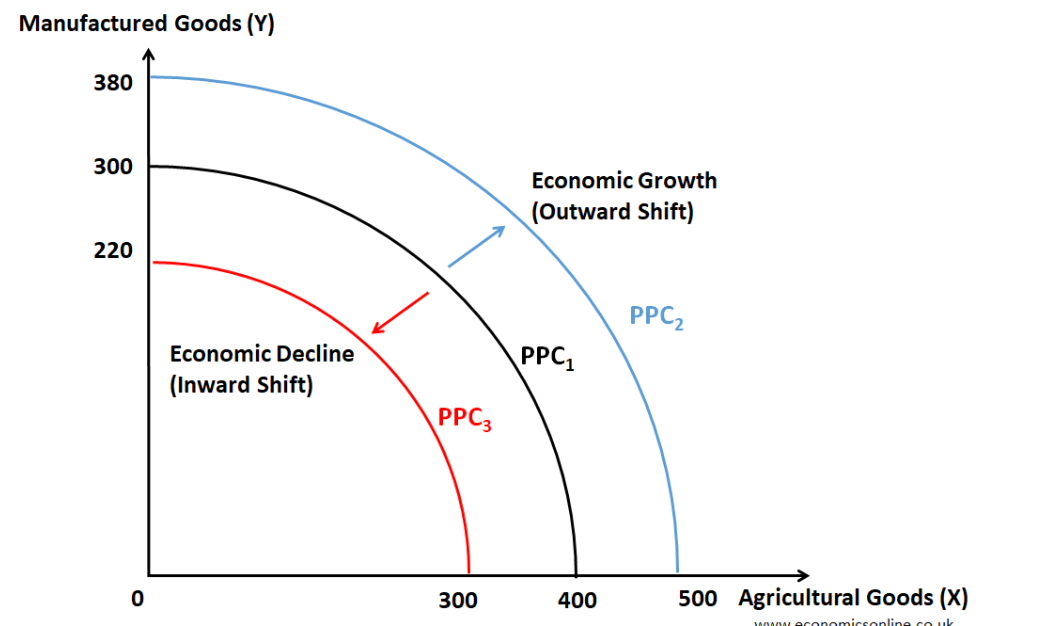

Changes in the PPF: Shift vs Rotation

1. Shift of the PPF (Parallel Movement)

A shift happens when a massive change impacts the production capacity of both goods at the exact same time. The entire curve moves parallel to its original position.

- Rightward Shift (Growth): The entire curve pushes outward. This is the ultimate goal of an economy; economic growth. It happens when a country discovers brand-new natural resources, experiences a population boom that increases the workforce, or invents a major technology (like AI or electricity) that upgrades all industries.

- Leftward Shift (Contraction): The entire curve shrinks inward toward the corner. This means the economy's maximum potential has been crippled. It happens during destructive events like wars, severe natural disasters, or pandemics that permanently destroy factories and reduce the active labor force.

2. Rotation in the PPF

A rotation is different. It happens when a technological breakthrough or a resource change alters production for only one of the two goods, while the other good's capabilities stay exactly the same.

- Rotation on the X-Axis : Imagine a massive technological upgrade happens only for the good in the X axis, then its production capability will increase.

- Rotation on the Y-Axis : If a new high-speed manufacturing method is invented solely for the good on the Y axis, then its production capability will increase.